If you get involved with the Inverse Finance DAO you will discover that a) there are some really talented people here and b) we spend time bouncing DeFi ideas around both to build out our product roadmap and even just for fun. One of the more serious product conversations, however, is challenging most of what we’ve assumed to be true or “correct” about DeFi lending. So we have been zooming in on ways to expand – exponentially, really – on the way we think about the way we borrow.

Variable rate lending in DeFi is the way things are done in DeFi. Yes, yes, there are some attempts at fixed rate lending but these amount to but a shadow of the TVL of variable rate lending.

But digging into the history of variable rate lending is … eye-opening.

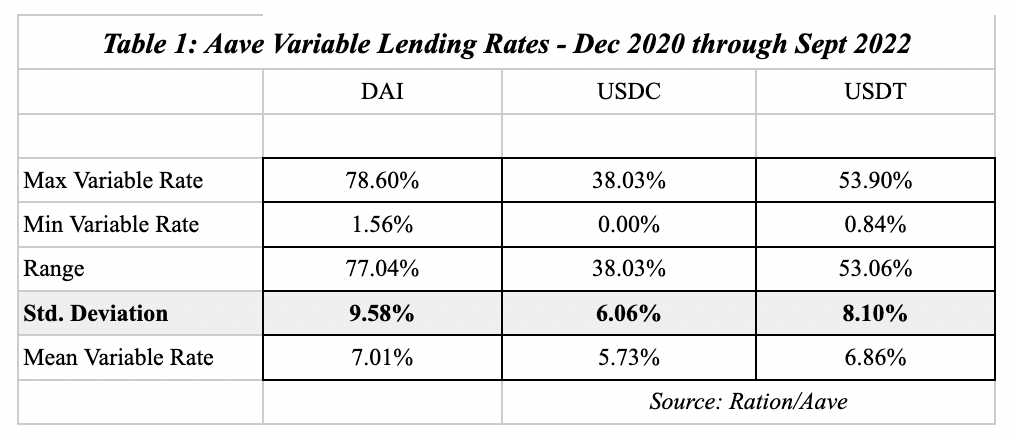

While volatility has calmed in recent months, overall from December 2020 to September 2022, variable rates are full of drama:

The range and standard deviation across DAI, USDC, and USDT variable rates are no less startling:

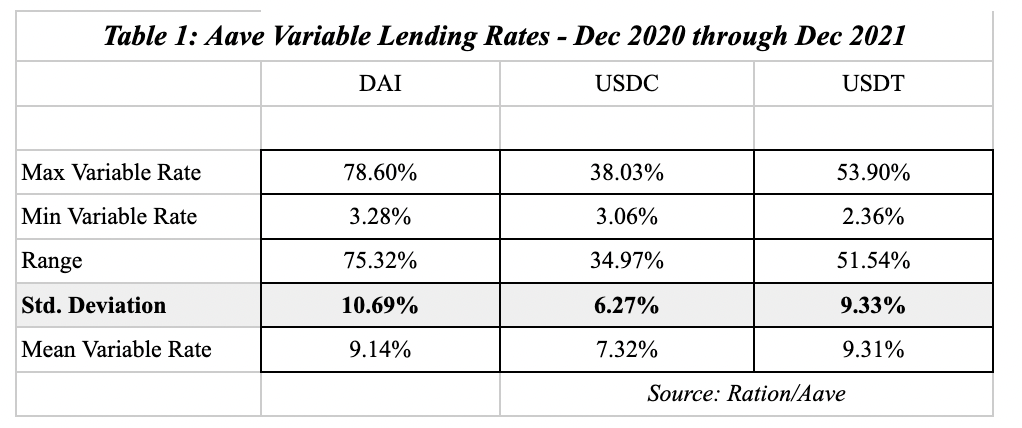

Controlling for the cooldown in 2022 and looking solely at 2021, which had its own May-June cooldown, more bullish conditions correspond with higher variable interest rate volatility:

Variable rates are volatile, but we are asking the question: will variable rate lending be the way we convert the TradFi world to DeFi? Variable borrowing rates that can zoom to 78% or that vary wildly on a day-to-day basis are unlikely to convince our TradFi friends that DeFi is the future.

For innovators and early adopter types who can stomach the volatility and engage in short-term trading, maybe there is no problem here. But for the much larger “early majority” segment that wants more predictability and lower borrowing expenses, such volatility remains a large barrier to DeFi adoption. If you are here to see DeFi transition from a “multi-billion” dollar to a “trillion-dollar” industry, we see a better way that turns everything you know about DeFi lending on its head. Looking forward to sharing more in the coming weeks.